There are multitudes of Life insurance policies and policy structures. Florida Protection Center, LLC has access to hundreds of insurance companies. Our goal is to guide our clients to an insurance company and policy that best fits their individual needs.

What Is Life Insurance

There are many varieties of life insurance. Some of the more common types are discussed below. We understand the complexities of design of the various types of life insurance policies and are here to help guide you to policies that may provide the coverage you are looking for.

There are many varieties of life insurance. Some of the more common types are discussed below. We understand the complexities of design of the various types of life insurance policies and are here to help guide you to policies that may provide the coverage you are looking for.

Term Life insurance

Term life insurance is designed to provide financial protection for a specific period of time, such as 10 or 20 years. With traditional term insurance, the premium payment amount stays the same for the coverage period you select. After that period, policies may offer continued coverage, usually at a substantially higher premium payment rate. Term life insurance is generally less expensive than permanent life insurance.

After that period, policies may offer continued coverage, usually at a substantially higher premium payment rate. Term life insurance is generally less expensive than permanent life insurance.

Needs it helps meet: Term life insurance proceeds can be used to replace lost potential income during working years. This can provide a safety net for your beneficiaries and can also help ensure the family’s financial goals will still be met—goals like paying off a mortgage, keeping a business running, and paying for college.

It’s important to note that, although term life can be used to replace lost potential income, life insurance benefits are paid at one time in a lump sum, not in regular payments like paychecks.

While most Term life policies expire at some point, some Term life policies have a return of premium benefit that returns the insured’s paid in premium in the event that they outlive their policy. Return of premium policies typically must be purchased at a younger age (usually prior to the age of 50).

WARNING: Not all Term life policies are equal and not all policies offer level premiums or coverage that will not change during the policy’s life. Other policies will cover accidental death only and will not cover you if the death is a result of an illness. The cheapest policy may not be in your best interest.

We are here to guide through the Term Life insurance maze.

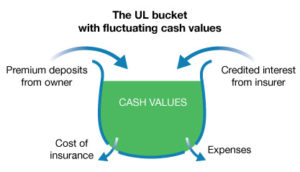

Universal life insurance

Universal life insurance is a type of permanent life insurance designed to provide lifetime coverage. Unlike whole life insurance, universal life insurance policies are flexible and may allow you to raise or lower your premium payment or coverage amounts throughout your lifetime. Additionally, due to its lifetime coverage, universal life typically has higher premium payments than term.

Needs it helps meet: Universal life insurance is most often used as part of a flexible estate planning strategy to help preserve wealth to be transferred to beneficiaries. Another common use is long term income replacement, where the need extends beyond working years. Some universal life insurance product designs focus on providing both death benefit coverage and building cash value while others focus on providing guaranteed death benefit coverage.

WARNING: Though Universal life is sold as a permanent lifetime policy, there are complexities and risks in some Universal life policies that can leave the insured facing much higher premiums at an older age with no cash value built up to continue the coverage.

Other Universal life policies guarantee enough cash value to keep the policy active until it matures, and still others that can be used to grow net worth if managed correctly.

We are here to guide you through the Universal Life complexities.

Whole life insurance

Whole life insurance is a type of permanent life insurance designed to provide lifetime coverage. Because of the lifetime coverage period, whole life usually has higher premium payments than term life. Policy premium payments are typically fixed, and, unlike term, whole life has a cash value, which functions as a savings component and may accumulate tax-deferred over time.

Needs it helps meet: Whole life can be used as an estate planning tool to help preserve the wealth you plan to transfer to your beneficiaries and some policies that pay the insured dividends which can be paid in cash or used to increase the coverage face amount.

Other types of whole life policies are designed to help with planning for the final expenses that are associated with funeral costs. There are even final  expense plans that offer coverage regardless of health. Final expense plans often limit the amount of coverage by design due to its stated purpose of final expense.

expense plans that offer coverage regardless of health. Final expense plans often limit the amount of coverage by design due to its stated purpose of final expense.

Let us guide you to the Whole Life insurance policy that best fits your needs.

1. Estate taxes may apply to insurance proceeds. Florida Protection Center, LLC does not provide legal or tax advice. The tax information contained herein is general in nature, is provided for informational purposes only, and should not be construed as legal or tax advice. Consult with an attorney or tax professional regarding your specific legal or tax situation. 2. Only variable universal life offers investment options; Florida Protection Center, LLC does not currently offer this type of coverage.